Invest. Grow.

Shape Tomorrow.

Invest. Grow.

Shape Tomorrow.

Global عربي

Global عربي

KSA عربي

Global عربي

KSA عربي

Global عربي

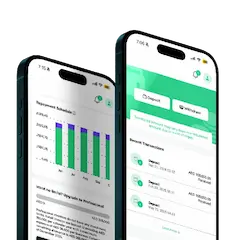

Funding Souq is a crowdfunding platform that connects established Businesses with Investors.

Download and register in seconds. Start investing right away.

Download Now

| empty |

Funding Souq

Private Credit

|

Real Estate

|

Stock Market

(S&P500)

|

High Yield Sukuk

or Bonds

|

|---|---|---|---|---|

|

Target Net Returns*

|

15% p.a | 8% p.a | 9.4% p.a | 6% p.a |

| Investment Horizon | As little as 3 months | Years | Varies | Varies |

|

Diversification

Low correlation to other asset classes

|

|

|

|

|

| Regular Monthly Income |

|

|

|

|

Funding Souq is a crowdfunding platform that connects established businesses with investors. The platform uses technology to connect both parties through the principle of crowdfunding, - i.e. raising small amounts of funds from many individuals.

Yes, Funding Souq is committed to offering investment and borrowing opportunities that align with the principles of Shariah. We are certified by Dar Al Sharia, a subsidiary of Dubai Islamic Bank. To view our Sharia certificated you can click here.

Simply put, investing with Funding Souq is one of the highest yielding investment options for retail and professional investors. Apart from the returns our investors benefit from:

1- Monthly Passive Income: Our investments repay principal and profit monthly, which enhances returns and decreases risk.

2- Data-Driven Decisions: Our credit risk teams use best in class credit models to ensure risk levels are kept to a minimum. Investors get a comprehensive profile of every investment opportunity.

3- Unique Opportunities: Gain exclusive access to investment opportunities in the UAE and Saudi Arabia. Funding Souq is the only crowdfunding platform that is regulated in both markets.

4-Low Barriers to Entry: Start investing with just AED 1,000 from almost anywhere in the world.

For businesses, our aim is to support you fulfill your potential by focusing on:

1-Quick Decisions: With our 3-day funding approval process, we are one of the quickest funders in the market.

2-Hassle-free Approach: No account opening is needed as we disburse the funds directly into your bank account.

3-Radical Transparency: We only charge a profit rate, an origination fee, and no other hidden fees unless a repayment is late. In this scenario we charge fixed late penalty fee as per the Shariah standards.

Debt-based crowdfunding, often referred to as peer-to-peer (P2P) lending, is a contemporary financing method where investors—both individuals and institutions—provide capital to businesses or other individuals via an online platform. In the case of Funding Souq, the beneficiaries are borrowers that are established businesses (SMEs).

An SME applies for funding either online or offline and then our experienced credit and compliance teams assesses the opportunity.

If approved, a funding request is launched on our Marketplace and investors have the opportunity to make an investment.

When the funding request gets filled, the funds are disbursed to the borrower. On the repayment date, the business is required to repay, and the investors can choose to re-invest or withdraw their funds.

Funding Souq ensures the security of information technology and data protection through robust measures, including encryption of sensitive data, periodic security audits, and compliance with regulatory standards on cyber security. The platform employs firewall protections, and intrusion detection systems, as well as Security Information and Event Management (SIEM) systems to monitor and analyze security events in real-time. Additionally, Funding Souq conducts regular employee training on cybersecurity best practices, performs ongoing monitoring and vulnerability assessments, and has a dedicated IT security team to respond to threats and maintain data integrity.